Europe’s stormwater infrastructure is nearing a critical breaking point, as decades of underinvestment, intensifying climate risks and urban expansion push flood damages to an average of €22bn annually.

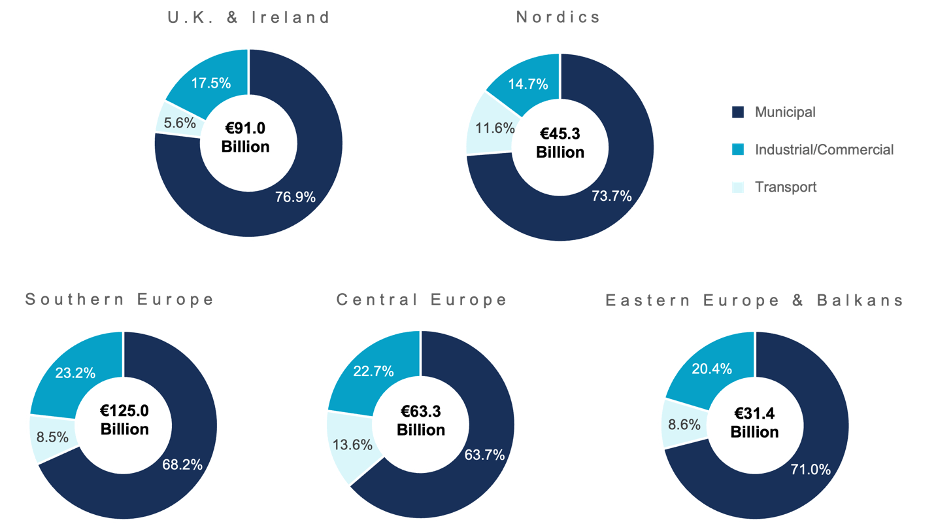

According to a new report by Bluefield Research, Europe stormwater infrastructure market: Key drivers, competitive shifts and investment outlook, 2026–2036, cumulative stormwater spending across Europe is projected to reach €643bn by 2036, growing at 1.7% annually. Yet current investment levels remain nearly 70% below what is needed to maintain basic service standards.

The report highlights how governments continue to rely on reactive spending following major flood events. Valencia issued €3.76bn in emergency tenders after a single flood, while Slovenia mobilised €7bn in reconstruction funding after severe floods in 2023 caused damages equivalent to 16% of its GDP. Since 1980, Europe has recorded more than €385bn in cumulative flood losses.

“European stormwater systems were designed for a climate that no longer exists,” said Antonio del Olmo, a senior analyst at Bluefield Research. “The last three decades rank among the most flood-intensive in 500 years, and for cities, this is now a crisis.”

Western Europe is expected to dominate cumulative capital expenditure through 2036, led by France with €92.9bn, the UK with €85.2bn and Germany with €73.9bn, driven by ageing assets and tightening regulatory obligations. Eastern Europe and the Balkans, while smaller in absolute spending, are projected to see the fastest growth as EU funding accelerates infrastructure upgrades and Green Deal compliance, according to the report.

Bluefield Research added that the competitive landscape remains fragmented across Europe, with procurement models and market access varying by geography. Mid-sized specialists including ACO Group, Hydro International, Hauraton and BIRCO continue to compete on product performance and regulatory compliance, benefiting from fragmented national standards that create strong defensive market positions.

Meanwhile, larger engineering and infrastructure firms such as Suez, Veolia, Arcadis, Arup, Ramboll, Sweco and Haskoning are leveraging their influence over project design and specifications to shape downstream technology adoption.

The report also identified digital stormwater management as one of the fastest-evolving segments. Established hydraulic modelling platforms from Autodesk, Bentley Systems and DHI are increasingly facing competition from cloud-native firms focused on real-time network management and predictive operations.

According to Bluefield, companies able to secure early positions within municipal procurement frameworks are likely to benefit from high switching costs and long infrastructure adoption cycles.

“This market is being built by necessity,” added Del Olmo. “Climate events are accelerating investment timelines, while the competitive positions established today will become increasingly difficult to displace as spending scales.”